Infectious Disease Diagnostics Industry Overview

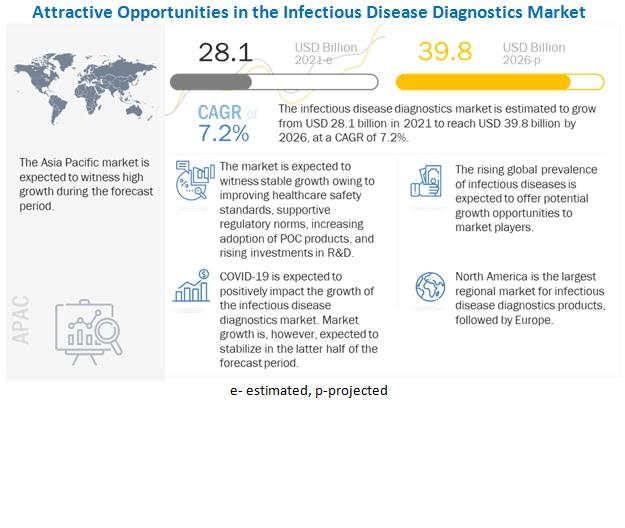

The global infectious disease diagnostics market size is projected to reach USD 33.1 billion by 2027 from USD 35.5 billion in 2022, at a -1.4% CAGR. The global prevalence of infectious diseases and the growing awareness for early disease diagnosis, shift in focus from centralized laboratories to decentralized POC testing and rising technological advancements are factors supporting the growth of this market. Growth opportunities in growing economies provide lucrative opportunities for the players operating in the infectious disease diagnostics market.

Gather more insights about the market drivers, restrains and growth of the Global Infectious Disease Diagnostics Market

Infectious Disease Diagnostics Market Segmentation

MarketsandMarkets has segmented the Digital therapeutics market on the basis of application, end user, and region:

The reagents, kits, and consumables segment accounted for the largest share of the infectious disease diagnostics market, by product & service segment, in 2021

Based on product & service, the infectious disease diagnostics market is segmented into reagents, kits, and consumables; instruments; and software & services. the reagents, kits, and consumables segment accounted for the largest share of this market.

POC testing segment to register the highest CAGR during the forecast period

Based on the type of testing, the infectious disease diagnostics market has been segmented into laboratory testing and POC testing. In 2021, the POC testing segment accounted for the highest CAGR. This can be attributed to the need to closely monitor patient conditions and advantages such as faster diagnosis.

The COVID-19 segment accounted for the largest share of the infectious disease diagnostics market, by disease type segment, in 2021

Based on disease type, the infectious disease diagnostics market is segmented into COVID-19, HIV, HAIs, hepatitis, CT, NG, HPV, Tuberculosis, influenza, syphilis, mosquito-borne diseases and other infectious diseases. In 2021, the COVID-19 disease type segment accounted for the largest share of this market due to factors such as the increasing number of cases and the availability of many COVID-19 diagnostic tests.

The diagnostic laboratories segment accounted for the largest share of the infectious disease diagnostics market, by end user segment, in 2021

Based on end user, the infectious disease diagnostics market has been segmented into diagnostic laboratories, hospitals & clinics, academic research institutes, and other end users. In 2021, diagnostic laboratories accounted for the largest share of the infectious disease diagnostics market.

Infectious Disease Diagnostics Regional Outlook

- North America

- Europe

- Asia Pacific

- Latin America

- MEA

COVID 19 Impact Analysis

COVID-19 is an infectious disease caused by the novel coronavirus. Largely unknown before the outbreak began in Wuhan (China) in December 2019, COVID-19 moved from a regional crisis to a global pandemic in just a few weeks. The World Health Organization (WHO) declared COVID-19 a pandemic on March 11, 2020.

Market Share Insights

- In November 2022, Roche Diagnostics Launched cobas 5800 system.

- In February 2021, Thermo Fisher Scientific acquired Mesa Biotech (US) to expand the benefits of molecular diagnostics at the point of care.

Key Companies Profile

The industry is marked by the presence of various large- and small-scale businesses operators. The market is highly competitive and dominated by key participants that focus on executing innovative strategies like mergers and acquisitions, market penetration, partnerships, and distribution agreements to increase their revenue.

Some prominent players in the global Infectious Disease Diagnostics market include,

- Abbott Laboratories (US)

- Hoffmann-La Roche Ltd. (Switzerland)

- Thermo Fisher Scientific Inc. (US)

- Siemens Healthineers AG (Germany)

- bioMérieux SA (France)

Order a free sample PDF of the Infectious Disease Diagnostics Market Intelligence Study, published by MarketsandMarkets